Very recently my colleague penned this wonderful article ‘A Gen Z Perspective on the Reinsurance Industry.’

It was a pinpoint (and rather bleak) assessment of a centuries old industry marred by inefficiency and doing things a certain way because 'that's the way it's always been done.'

This, from someone who’s relatively new to the industry, couldn't have hit the proverbial nail any squarer on its head.

And it got me thinking.

As an early-to-mid career professional with nearly a decade's worth of experience, what's a millennial's assessment of the reinsurance industry, and more specifically, reinsurance technology?

First, I’ll tell you why it’s important.

Millennials will represent 75% of the global workforce by 2025 - and companies in all sectors, including reinsurance, will need to consider our needs and expectations if they want to attract and retain the best talent.

To give you some experiential context to frame our article, let me provide background on how I came to join the industry.

I Left a 165 Year Old Reinsurer to Join a Reinsurance Technology Startup

My career began in 2014 at HSB - Hartford Steam Boiler as an internal business analyst, working my way up through the organization to become a Client Company Manager.

I grew a book of assumed reinsurance clients from $800K to $20M in Annual Gross Written Premium in just 4 years.

HSB is widely credited as the founder of assumed reinsurance - it’s safe to say I was lucky to have learned from some of the best.

I'm sure the insurance nerd inside of you is wondering, what is assumed reinsurance?

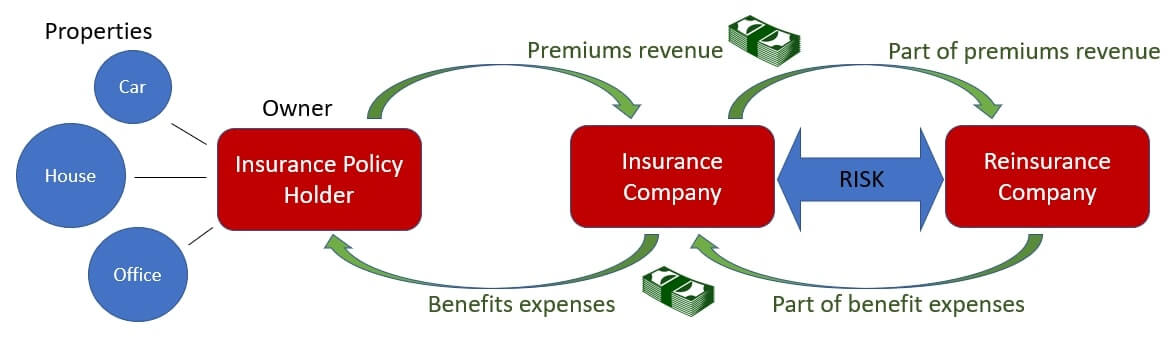

Plainly put, one insurance company (IC) who writes a reinsurance program of, say, hotels and bars, underwrites certain specialty insurance coverages for those businesses on behalf of another company - the reinsurer.

Here's a great diagram that breaks down a typical reinsurance workflow:

Credit: Harvard Business Review

These reinsurers, like HSB, are basically outsourced experts that provide the specialty coverages.

They handle the claims specific to their coverages, transfer 100% of the related risk from the writing companies' balance sheet to the reinsurer, and deliver a more robust product offering to the end insurer.

But it can get pretty complicated: reinsurance can come in various structures and types

This presents a huge problem when it comes to managing programs across the reinsurance value chain, particularly with the technology available.

Let me explain.

The Reinsurance Technology Problem

As you can imagine, reinsurance is quite an arduous process with many, many moving parts.

After all, it's not easy for an insurance company to write a reinsurance product (especially if we're talking about admitted regulated business).

Development, rate filings with the department of insurance, claims handling procedures, IT and coding, internal systems, policy administration.

I was personally responsible for quarterbacking and managing the necessary teams and departments for many of these things - very much the Tom Brady of reinsurance (apologies to my non-US colleagues for the football - not soccer - references 😅).

In my experience, there’s one key to unlocking proper analysis and exchange of an IC’s book of business:

Good data.

Unfortunately, most data prep is performed using legacy technology.

Cue the circus theme music.

If you’re reading this article I assume you’re familiar with the pain of H lookups and V lookups of thousands of rows of data.

Experienced scrolling through 2 year-old email chains to extract data? Again, because, same.

It was a very challenging and manual process to aggregate hundreds of gigabytes of spreadsheets, Word docs, and PDF's, and get them into an acceptable format that the profiling and corporate -underwriting teams could process.

It required tremendous effort just to get the data right; we won't mention the internal modeling or proprietary system workflows that followed.

Keep in mind, the process by which the data was aggregated and shared was different according to each individual company.

Imagine!

Those files were often piecemeal; found across various sources - legacy databases and custom built programs; email and Excel sheets with broken formulas - there was no singular version of the truth, but many versions of some truth.

Lotus Notes (about as archaic as a payphone) was the preferred methodology of client management systems - if you're in your mid 30's or younger, you'll likely have to Google it.

Let's fast forward to January of '22 when I joined Supercede as the Director of Business Development for North America.

I’ll tell you why I made the jump.

The Reinsurance Technology Solution

When I was initially presented with the opportunity to join the Supercede team, I was able to see the platform work in real time prior to joining.

I knew instantly that this tool was going to fundamentally change reinsurance.

I remember thinking to myself:

What if I had this tool in my day to day at HSB? How much more efficient could this make me, and impact my clients?

Frankly, I'd be just fine if I never had to use another spreadsheet again in my career.

I recently saw a study that showed up to 80% of spreadsheets have errors - this doesn’t surprise me.

Hundreds of countless hours are lost and wasted (amongst so many other inefficiencies when using combinations of multiple legacy and new systems) in the reinsurance workflow manually massaging the previously aforementioned spreadsheets and documents.

Supercede changes all of that.

It’s the only platform I know of that works to incorporate and connect the entire tripartite value chain of insurers (aka cedents), reinsurance brokers, and reinsurers.

Cedents analyze and validate necessary underlying reinsurance information then selectively share that information to reinsurance brokers.

And this is all on one platform.

Brokers, working in concert with reinsurers, seamlessly place the reinsurance in real-time on a web-based platform.

I was blown away seeing this for the first time. And a little annoyed no one had made the effort to invest in creating better reinsurance technology before!

The headache of renewal season and days of janitorial data cleansing are gone forever.

Our reinsurtech platform saves invaluable time and energy across the entirety of the reinsurance workflow, with research showing up to an 85% reduction in data prep time, as well as a 20% reduction in overall admin costs.

Saving ~3 weeks in time preparing exposure profiles is a serious return on investment.

I'm always one for a good reinsurance meme 🤓😹

So What’s This Millennials’ Assessment of Reinsurance Technology?

It's a C+ for me (prior to Supercede, of course!).

For an industry that prides itself on its longstanding ability to weather the storm (CAT XOL's anyone? ), it is far behind on the technological and operational efficiency spectrum (specifically reinsurance).

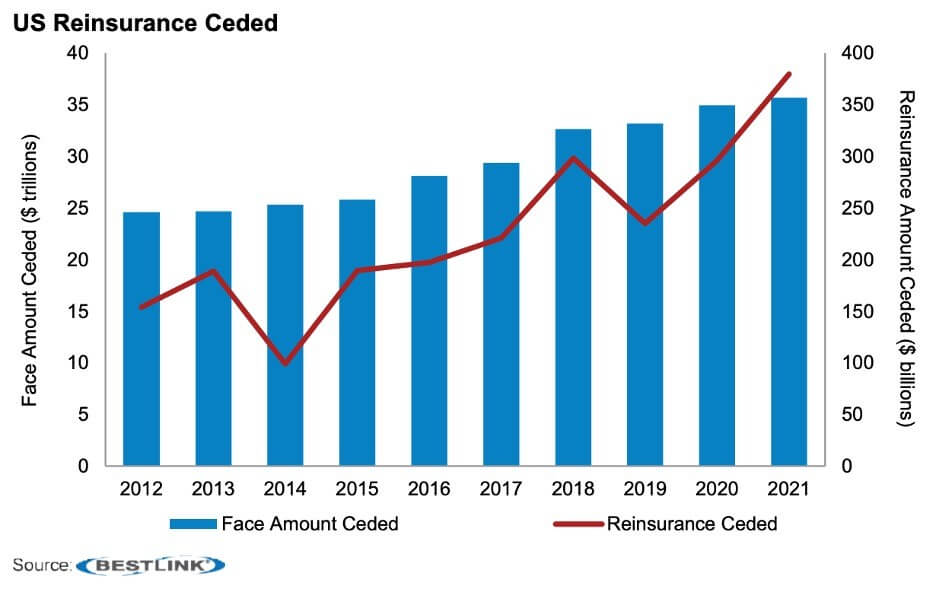

The reinsurance industry is going nowhere soon, with nearly $400B in premiums ceded in 2021, with the trend line pointing upwards.

(Although the extreme difficulty of this past renewal season might impact this.)

Credit: BESTLINK via A.M. Best

Established players, however, could be under threat from the likes of traditional tech companies looking to diversify into the world of insurance.

Apple, Tesla, and Google are competing now more than ever with traditional insurance companies and insurtech players (all three have some type of insurance product and/or distribution play).

Companies industry wide throughout the market are no longer immune to traditional barriers of entry like capital, and regulatory requirements.

Firms of all shapes and sizes are figuring it out, and will figure out how to do it better, faster, and cheaper, it's only a matter of time.

Re/insurance companies have to keep pace.

Insurtech Is Nothing New to the U.S. Market, Reinsurtech However…

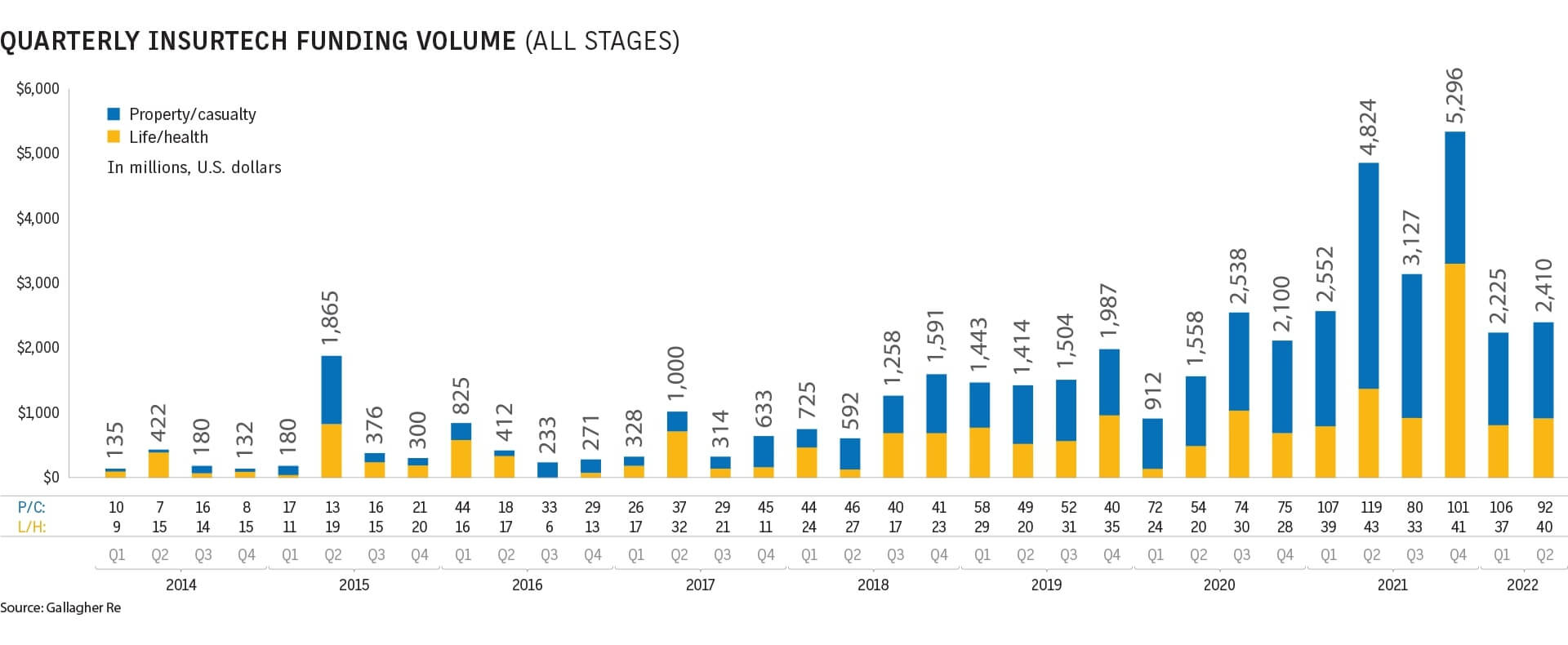

I’d consider insurtech a maturing and saturating market, as evidenced by this November insurtech report from the wonderful Dr. Andrew Johnston of Gallagher, and noted in the Business Insurance chart below.

Credit: Business Insurance

For those counting, that's almost $5bn USD in InsurTech investment through 1H 2022.

However true, I think this more-so applies to those startups looking to enter the industry and existing companies.

While new insurtech deal size has shrunk considerably, there is still a myriad of capital being dished out, even with a renewed focus on profitability as opposed to growth.

The reinsurtech sector, however, is a new and booming industry.

In this last renewal season of 22’/23’, over $24bn USD of reinsurance premium was placed through our platform.

For the HSB's, Markel's, and Aon's of the world, myriad solutions and efficiencies are to be gained from partnering with various reinsurtech solution providers, throughout their operational workflows.

So, why haven't more companies automated their back of house re/insurance operations?

Sometimes, companies just don’t know how to buy reinsurance software.

Ultimately, it stands to benefit both the company and the end insured - the most important piece of the puzzle.

Companies become more efficient, decrease their overhead, and make it more cost-effective for the insured.

The industry is increasingly embracing reinsurtech to improve efficiency, reduce costs, and enhance risk management.

These are the key areas where reinsurtech assists practitioners:

- Automation: Automation of manual processes such as underwriting, claims handling, and accounting can greatly improve efficiency and reduce costs.

- Big Data and Analytics: The use of big data and analytics is helping reinsurers better understand and manage risks. Advanced analytics can be used to identify patterns and trends in data, which can be used to improve underwriting, claims management, and risk management.

- Cloud computing: Cloud computing is allowing reinsurers to access powerful computing resources on-demand, which can be used to process large amounts of data, run complex simulations, and support advanced analytics.

- Artificial intelligence and machine learning: Reinsurers are also experimenting with AI and machine learning to improve underwriting, claims management, and risk management.

Overall, the reinsurance industry is becoming more digitized, data-driven and technology-focused, which is helping companies to make better decisions.

While the reinsurance industry is alive and well, it's the proverbial old dog that will have to learn some new tricks to stay ahead of the innovation curve, and reinsurtech platforms like Supercede appear to be the best trainer to help.

TLDR: Reinsurance companies are wildly inefficient in their workflows and operations. Partnering with reinsurance technology companies like Supercede benefits everyone involved in the distribution channel.